{ Full Bloomberg Article Here }

Apartment prices prove most linked to jobs growth in the U.S.

Greedy landlords or just plain jobs growth?

A new Morgan Stanley analysis sheds some pictorial light on America’s rising rents.

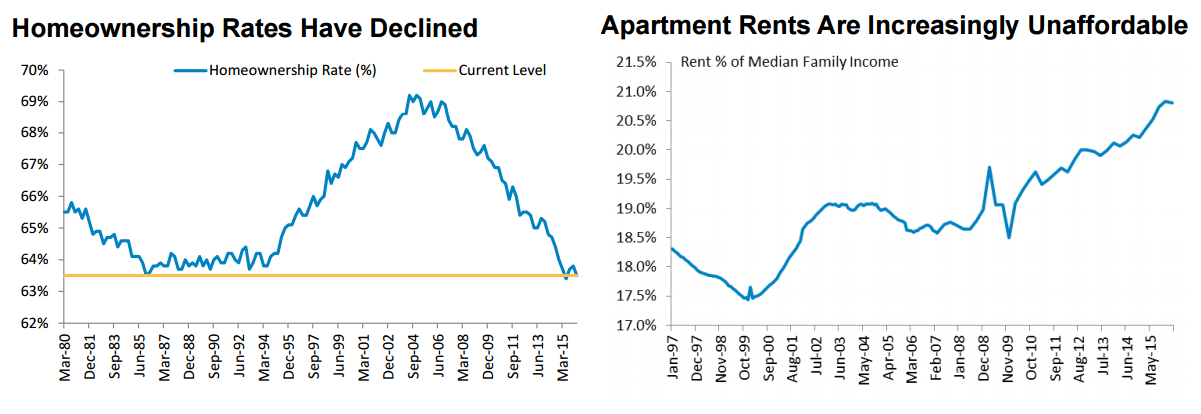

Home ownership rates in the U.S. have plummeted to a near five-decade low in the aftermath of the U.S. housing bubble, leaving millions of Americans to rent apartments instead of buying houses. Some 2.5 million households shifted into multifamily properties between 2009 and 2014, according to data put together by Morgan Stanley’s Richard Hill and Jerry Chen, while the number of owner-occupied homes fell by 850,000.

Soaring demand for apartments means pressure on prices with historical data from 36 Metropolitan Statistical Areas (MSAs) showing that rents are growing above their long-term average rate — at 5.2 percent currently vs. 3.0 percent. The rent component of the Consumer Price Index is at 3.8 percent year-on-year, a level not seen since 2008. The surge means rental expenses now comprise 20.8 percent of median family income.

While the following is likely to provide little comfort to Americans struggling to pay the rent, Morgan Stanley finds that specific rent inflation is linked to macroeconomic trends including employment growth, income, jobs supply, and vacancies. Among those variables, jobs growth is by far the strongest link with a correlation coefficient of 0.75 compared to 0.60 for jobs supply, 0.57 for vacancy rates, and 0.56 for income growth.

On that basis, renters in Dallas, Austin, Orlando, Richmond, and Phoenix — the five MSAs showing the strongest jobs growth — might be first in line for an unwelcome visit from their landlords.